The 48-Hour Repricing: What a Legal Plugin Taught Banking About Its Software Future

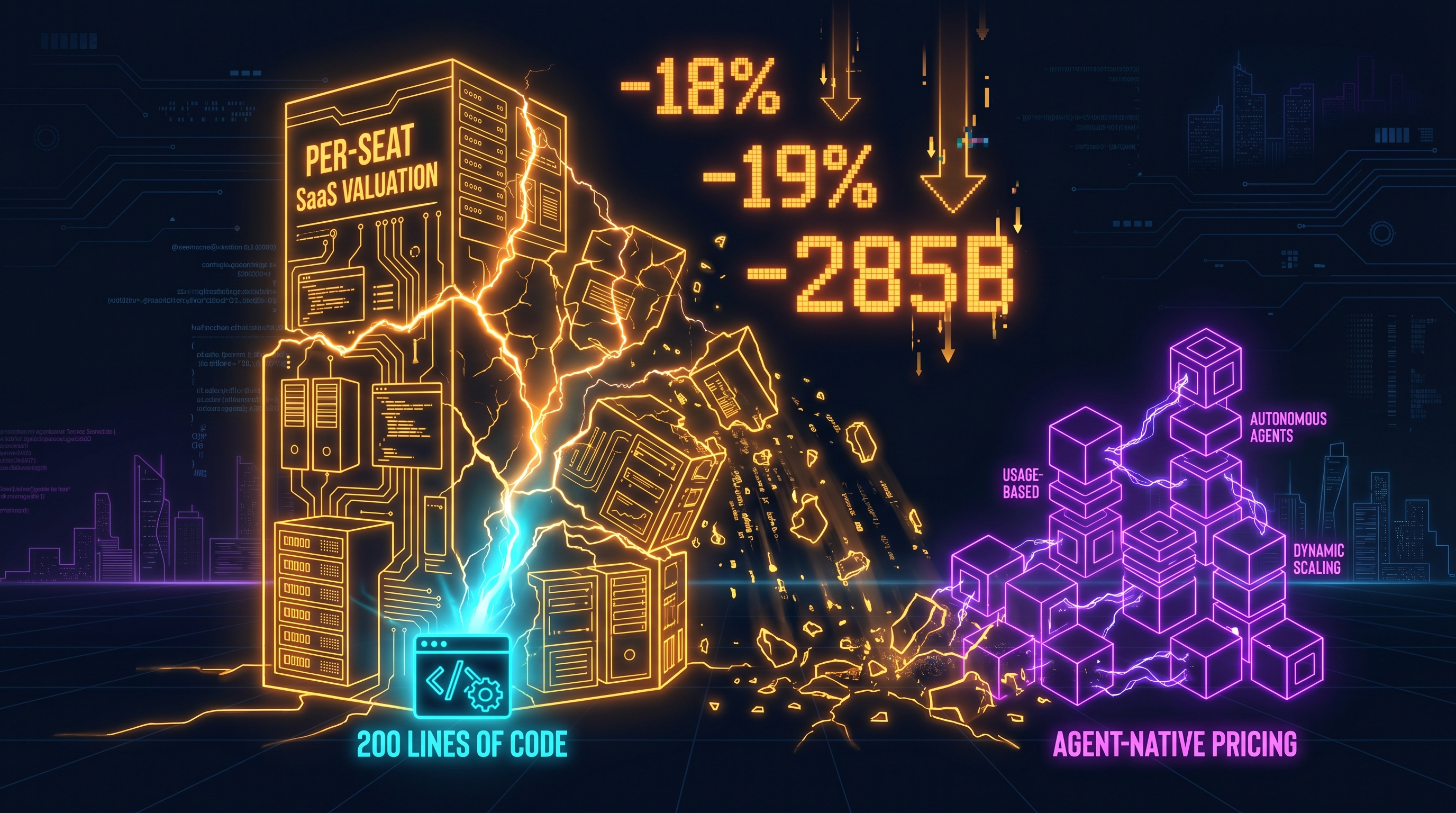

Two hundred lines of code. That’s all it took.

On February 2, 2026, Anthropic released a legal research plugin for Claude. Not a product launch. Not a platform shift. A plugin: one narrow vertical capability bolted onto an existing AI model. Within 48 hours, Thomson Reuters dropped 18%, RELX fell 14%, LegalZoom cratered 19.2%, and $285 billion in software market cap evaporated.

The legal industry was the target. But if you work in banking technology, you should be paying closer attention than anyone.

The Per-Seat Model Was Already Dying

The crash didn’t happen because a plugin replaced lawyers. It happened because the market suddenly understood what AI agents mean for software pricing.

The per-seat SaaS model assumes a human sits behind every license. An analyst uses Bloomberg. A loan officer uses nCINO. A compliance officer uses Archer. One human, one seat, one recurring revenue line. The entire software valuation framework, recurring revenue times a growth multiple, depends on that assumption holding.

AI agents break it. An agent that processes loan applications doesn’t need a seat. An agent that monitors transactions for suspicious activity doesn’t need a seat. An agent that drafts regulatory filings doesn’t need a seat. When the work gets done without a human in the loop, the seat vanishes, and the revenue model vanishes with it.

The market had been slowly digesting this. Software P/E ratios compressed from 39x to 21x over roughly eight months: the steepest sustained compression since 2002. But the legal plugin made the abstract concrete. A single capability demonstration triggered the fastest repricing event the software sector has ever seen.

Banking’s Different Math, and Why It’s Worse

Here’s where it gets interesting for financial services.

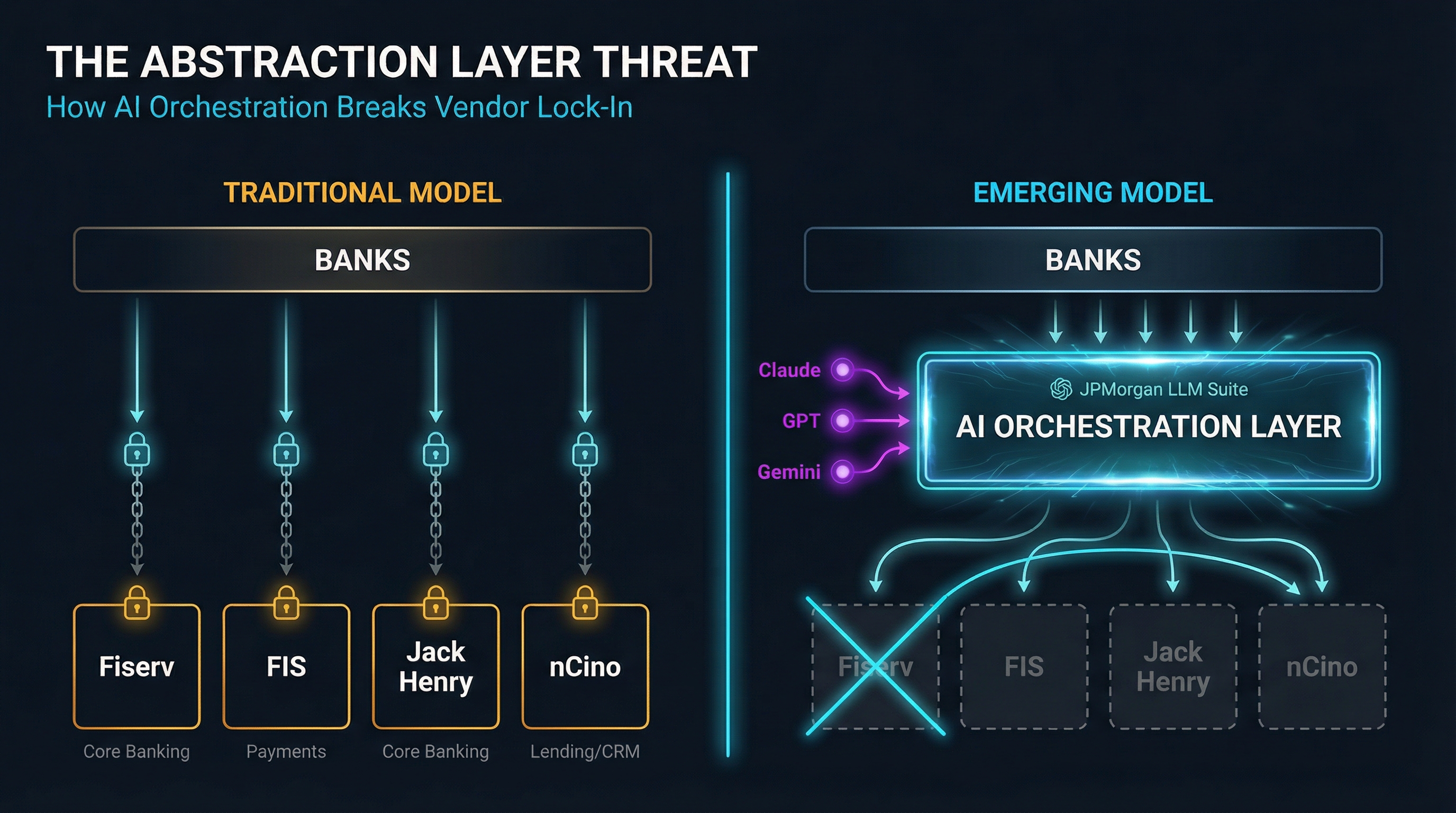

US core banking runs on three vendors: Fiserv, FIS, and Jack Henry. Together they process the vast majority of American banking transactions. Their pricing model is enterprise licensing per bank, not per seat. A community bank pays Fiserv based on asset size and transaction volume, not how many tellers log in. On the surface, this looks insulated from the seat-collapse dynamic.

It’s not.

The Salesforce Financial Cloud ecosystem, with nCINO as a key component for lending workflows, sits closer to the per-seat model. Loan officers, relationship managers, and branch staff each represent a seat. When AI agents start handling loan origination workflows end-to-end, those seats become harder to justify at current pricing.

But the real threat isn’t about seats at all. It’s about what the biggest banks are building internally.

JPMorgan now has 200,000 employees on its internal LLM Suite, a model-agnostic AI platform running on AWS. They’re spending $18 billion annually on technology and have deployed over 450 AI use cases. Goldman Sachs is scaling thousands of AI software engineers and reporting 3-4x productivity gains. Citi is seeing 2-20x productivity improvements with AI agents across operations.

When the largest buyers of banking technology start building their own AI abstraction layers, the vendor relationship changes fundamentally. JPMorgan isn’t just using AI tools. They’re building the orchestration layer that decides which tools matter, and which ones don’t.

The Abstraction Layer Threat

This is the dynamic that should keep banking software executives up at night.

A model-agnostic orchestration layer does something no single vendor product can: it makes vendors interchangeable. JPMorgan’s LLM Suite doesn’t care whether the underlying model is Claude, GPT, or Gemini. It abstracts the AI capability away from any single provider. Today that abstraction sits above AI models. Tomorrow it sits above everything: core banking, lending platforms, risk engines, compliance tools.

When a bank can orchestrate its own AI capabilities across any combination of models and services, vendor lock-in dissolves. The switching cost that protected Fiserv’s margins, the sheer complexity of migrating core banking systems, starts to erode when an intelligent orchestration layer can wrap, replace, or route around any individual component.

Only 2% of financial institutions report no AI use at all, according to Finastra’s 2026 survey. And 57% of banks are allocating 21-50% of their technology budgets specifically to AI automation. This isn’t experimentation anymore. It’s infrastructure-level commitment.

The question isn’t whether banks will build internal AI platforms. They already are. The question is what happens to Fiserv, FIS, Jack Henry, nCINO, and every other banking software vendor when their largest customers can replicate or route around their core capabilities through an AI orchestration layer.

What Survives, What Dies

Not everything is equally exposed. The software that survives this transition has one thing in common: it provides something AI orchestration can’t easily replicate.

Data assets hold. Thomson Reuters lost 18% on the legal plugin news, but their underlying legal databases (decades of case law, regulatory filings, proprietary datasets) remain valuable regardless of the delivery mechanism. In banking, vendors who own proprietary data (transaction networks, credit histories, regulatory databases) retain leverage even as the software layer commoditizes.

Accountability holds. Regulated industries need someone to sue when things go wrong. A vendor who provides a regulated, auditable, contractually liable service occupies a different position than a vendor who provides a tool. When the OCC asks who’s responsible for a lending decision, “our internal AI agent” is a harder answer than “our licensed vendor platform.”

Pricing models die. Per-seat, per-user, per-login: any model that counts humans as the unit of value is structurally exposed. The transition to consumption-based, outcome-based, or platform-licensing models is no longer optional.

Delivery-only value dies. If your product’s primary value is packaging capabilities that AI can now provide directly, the legal plugin just showed you your timeline. The difference between “using AI tools” and “rethinking workflows around AI capabilities” is the difference between incremental improvement and structural transformation.

The Incomplete Picture

I don’t have a clean conclusion here, and I think that’s honest.

The $285 billion repricing happened in 48 hours. The banking industry’s response will take years. JPMorgan is further along than most community banks will be in a decade. The regulatory environment creates genuine friction that slows adoption. As I explored in The Compliance Tax, regulated industries pay a real productivity penalty that tempers the disruption timeline.

And the technology friction inside banks is substantial. Access controls, change management, audit requirements: these aren’t going away just because AI agents are getting capable.

But the direction is clear. Every major bank is building internal AI orchestration. Every quarter, the capability gap between what these platforms can do and what external vendors provide narrows. Every new AI release, every legal plugin, every coding agent, every autonomous workflow, compresses the adaptation window.

The 48-hour repricing wasn’t a market overreaction. It was the market catching up to a structural shift that’s been building for months. Banking software vendors who treat it as someone else’s problem are making the same mistake the legal technology companies made: assuming the wave would hit a different shore.

If you’re navigating this shift in financial services, I’d like to hear your perspective. Find me on LinkedIn or X.